Published for North Alabama home sellers | Updated 2026 | Serving Huntsville, Madison, Athens, Limestone County, Ardmore & Decatur

The Quick Answer (TL;DR)

If you’ve been wondering how to price a house in Huntsville or anywhere in North Alabama, here’s the short version: the right price is the highest number the current market will actually support — not the number that makes you feel good, and not a round figure you picked from Zillow’s estimate. It’s a data-driven conclusion anchored to recent comparable sales, your home’s condition, and where buyer demand sits right now in your specific submarket.

Price it right from day one and you’ll attract more buyers, generate more competition, and very likely close at or above list price. Price it wrong — even by 3–5% — and you’ll sit on the market long enough to lose that advantage entirely.

→ New to the selling process? Start here first: Huntsville Home Selling Timeline: How Long Does It Really Take?

What’s Happening in the Local Market (Huntsville / Madison / Athens)

Pricing strategy doesn’t exist in a vacuum — it’s shaped entirely by local conditions. Here’s what North Alabama sellers need to understand about the current market landscape before they ever pick a number.

Huntsville

Huntsville is the MSA anchor and the most price-competitive submarket. Buyer demand has been consistently strong, supported by Redstone Arsenal expansion, the growing aerospace and defense technology sector, and ongoing corporate relocations. Well-priced homes in South Huntsville, Hampton Cove, and Research Park corridor neighborhoods still attract competitive offers. However, the higher price points — particularly above $500K — have softened relative to the pandemic-era peak, meaning accurate pricing matters more than ever at upper price brackets.

Madison & Madison City Schools District

Madison remains one of the most demand-driven submarkets in North Alabama, largely because of the Madison City Schools district. Homes within district boundaries consistently command a premium over comparable homes just outside it — sometimes $15,000 to $30,000 or more at similar square footage. If your home feeds into Madison City Schools, that’s a pricing lever your CMA needs to reflect. If it doesn’t, pricing against Madison City comps is one of the most common and costly mistakes sellers in surrounding zip codes make.

Athens & Limestone County

Athens and the broader Limestone County market have seen meaningful appreciation driven by Toyota’s manufacturing expansion and the spillover of buyers priced out of Madison and Huntsville. Days on market here tend to run slightly longer than in Madison, but well-prepared and well-priced homes are moving. The key in this market is understanding that buyers relocating for Toyota and nearby employers are often comparing multiple communities simultaneously — price needs to be compelling relative to what they can get in Madison for the same money.

Ardmore & Decatur

Ardmore and Decatur represent the outer edges of the North Alabama market where price sensitivity is highest. Buyers in these areas are highly attuned to value — they’re comparing what their dollar buys here versus in a closer-in community. Overpricing in these markets produces disproportionately long days on market because the buyer pool is smaller and comparison shopping is more deliberate.

How to Price Your Home: A Step-by-Step Approach

Step 1: Understand the Difference Between a CMA and an Appraisal

These two terms get conflated constantly — and confusing them leads to bad pricing decisions.

A Comparative Market Analysis (CMA) is prepared by your listing agent. It analyzes recent sales of comparable homes in your area — similar size, condition, age, and location — and uses them to establish a probable market value range. A good CMA is the foundation of your pricing strategy.

An appraisal is a formal valuation conducted by a licensed appraiser, typically ordered by a buyer’s lender after a purchase contract is signed. It’s not the same as a CMA, it doesn’t happen before you list, and it isn’t designed to help you choose a list price.

The important intersection: if you price above what the market will appraise at, a financed buyer’s deal may fall apart even after you’ve accepted their offer. This is why a CMA anchored to appraisal-compatible comps matters. For more on this, the CFPB’s home selling resources offer a useful overview of how lender appraisals work in a purchase transaction.

Step 2: Pull the Right Comparable Sales

The quality of your CMA is only as good as the comps it’s built on. Here’s what makes a comp valid in the North Alabama market:

- Sold within the last 90 days — anything older starts to reflect a different market

- Within 0.5 to 1 mile of your property when possible, or within the same subdivision or school district

- Similar square footage — within 10–15% of your home’s finished living area

- Similar age, style, and condition — a 2005 brick ranch doesn’t comp well against a 2022 craftsman

- Same bedroom/bathroom count or within one of each

- Similar lot size, garage configuration, and key features (pool, finished basement, etc.)

In fast-moving submarkets like Madison City Schools neighborhoods or Liberty Park, even 90-day-old comps can be stale. Your agent should flag this and weight more recent sales more heavily when the market has been moving.

Step 3: Understand Your Market Absorption Rate

Absorption rate tells you how fast homes are selling in your specific price range and area. It’s calculated by dividing the number of active listings by the number of homes sold per month — the result is the number of months of supply currently on the market.

| Months of Supply | Market Condition | Pricing Implication |

| Less than 3 months | Seller’s market | Pricing at the top of your range is justified — demand exceeds supply |

| 3–6 months | Balanced market | Price at fair market value — neither aggressive nor conservative |

| More than 6 months | Buyer’s market | Price competitively or buyers will simply wait you out |

Your agent should pull absorption rate data specific to your price band and zip code — not just the overall Huntsville metro. A balanced market at the metro level can still be a strong seller’s market in Madison City Schools and a buyer’s market in a slower Decatur price range simultaneously.

Step 4: Evaluate Your Home’s Condition Honestly

Market data tells you what similar homes are worth — your home’s condition determines where within that range you actually land. Buyers apply an implicit discount for deferred maintenance, dated finishes, and anything that signals work ahead of them. That discount is almost always larger in their heads than it would cost you to address.

The honest condition assessment covers:

- Roof age and condition — buyers and their inspectors will find this regardless

- HVAC age — a system over 12–15 years old creates buyer hesitation at full-price offers

- Kitchen and bath finishes — not whether they’re updated, but whether they’re competitive with what else is for sale at your price point

- Flooring condition throughout

- Curb appeal and exterior condition — this shapes buyer psychology before they step inside

- Any known issues: foundation, drainage, electrical, plumbing

→ For a complete pre-listing prep list tied to ROI: Pre-Listing Checklist: 21 Things That Increase Your Sale Price (ROI First)

Step 5: Factor In Buyer Psychology and Search Thresholds

Buyers on Zillow, Realtor.com, and the MLS search by price range — and those ranges have hard ceilings. Pricing your home at $305,000 means you’re invisible to every buyer whose search tops out at $300,000. Pricing it at $299,900 puts you in front of the entire pool searching up to $300,000 AND buyers searching $275,000–$300,000 on overlapping filters.

Common price threshold bands to be aware of in the North Alabama market:

- $200,000 / $225,000 / $250,000 — entry-level and first-time buyer thresholds

- $275,000 / $300,000 — move-up buyer sweet spot in Athens and outer Limestone County

- $325,000 / $350,000 — competitive Madison and South Huntsville range

- $400,000 / $425,000 / $450,000 — Madison City Schools premium tier

- $500,000+ — upper tier where appraisal risk increases and buyer pool narrows

Step 6: Set Your List Price and Know Your Bottom Line

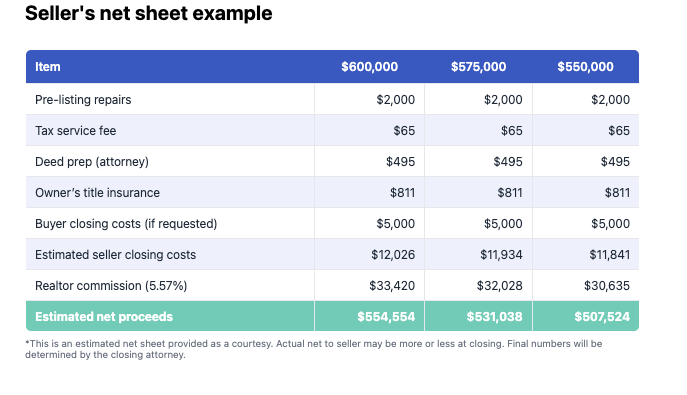

At the same time, make sure you have a completed seller’s net sheet before you goWith your CMA, absorption rate, condition assessment, and threshold analysis in hand, you’re ready to set a list price. Your agent should present a range — a floor and a ceiling — and help you choose a number within it based on your specific goals: fastest sale, highest price, or a balance of both.

live. This is a line-item estimate of what you’ll actually walk away with after commissions, closing costs, pro-rated taxes, and mortgage payoff. Knowing your bottom line before you get offers means you can evaluate each offer confidently rather than reactively.

→ Seller Net Sheet Explained: What You’ll Actually Walk Away With

Quick Pricing Checklist Before You Go Live

| Pricing Readiness Checklist ✅ CMA completed with comps from the last 90 days (60 days in fast-moving submarkets) ✅ Absorption rate pulled for your specific price range and zip codeSchool district confirmed and factored into comp selection ✅ Condition assessment completed — known issues priced in or disclosed Price threshold analysis done — no accidental search filter cliffs ✅ Seller’s net sheet reviewed and bottom line confirmed ✅ List price reviewed against likely appraisal range for financed buyers ✅ Competing active listings reviewed — you’re pricing against them, not just sold comps |

Common Home Pricing Mistakes (And How to Avoid Them)

Mistake #1: Pricing Based on What You Need, Not What the Market Supports

What you paid for the home, what you owe on it, what you need for your next down payment — none of these facts are known to buyers, and none of them affect market value. The market doesn’t care about your financial situation. It only cares about what comparable homes have sold for recently. Starting your price from a personal financial target and working backward almost always results in overpricing.

Mistake #2: Trusting Automated Valuations (Zestimates) Without Context

Zillow’s Zestimate and similar automated valuation models (AVMs) use public record data and algorithm-based adjustments. They don’t know your home’s condition, they don’t account for recent updates or renovations, and they frequently lag behind fast-moving local markets. In North Alabama — where a school district line can change values by $20,000+ on the same street — AVMs are particularly unreliable. Use them as a very rough starting point, never as a pricing basis.

Mistake #3: Leaving Room to Negotiate by Padding the Price

“I’ll price it high and come down if I need to” is one of the most expensive strategies in real estate. Overpriced homes attract fewer showings because buyers’ search filters eliminate them. The buyers who do visit already suspect something is wrong. By the time you reduce the price, you’ve accumulated days on market that signal weakness and invite lowball offers. Buyers who would have paid full asking price in week one will offer less in week four after watching the price sit.

Mistake #4: Ignoring the School District Effect

In the Huntsville metro, school district assignment can swing comparable home values by 10–20% on otherwise identical properties. Madison City Schools, Huntsville City Schools, and Limestone County Schools all carry different buyer demand levels. If you’re in a desirable district, not pricing to reflect it means leaving real money on the table. If you’re pricing your home against comps from a higher-demand district you don’t feed into, you’ll sit.

Mistake #5: Skipping the Active Listings Analysis

Your competition isn’t homes that already sold — it’s homes currently for sale that buyers will view alongside yours. A CMA built entirely on sold comps without reviewing active listings can miss the fact that three similar homes just came on the market at lower prices. Buyers will compare you directly to those listings before making any offer.

Frequently Asked Questions

How do I know what my home is worth in Huntsville, AL?

The most reliable way to determine what your home is worth in Huntsville is a Comparative Market Analysis (CMA) prepared by a local listing agent with recent transaction data in your specific neighborhood. Online estimates from Zillow or Redfin are a rough starting point but frequently miss local nuances — school district premiums, condition adjustments, and submarket demand shifts — that can move your value by tens of thousands of dollars. A certified appraiser can also provide a formal valuation, which is particularly useful for estate, divorce, or FSBO situations.

Should I price my home high and come down, or price it right from the start?

Price it right from the start — without exception. Homes that launch at the correct price generate the most traffic in the critical first two weeks, when buyer interest is highest and the listing is algorithmically boosted as new on major portals. Overpriced homes sit, accumulate days on market, and ultimately sell for less than they would have if priced correctly at launch. The data on this is consistent across markets and price points.

How does the Madison City Schools district affect home pricing?

Significantly. Homes within the Madison City Schools district consistently command a meaningful premium over comparable homes in adjacent districts — often $15,000 to $30,000 or more at similar square footage and condition. When pulling comps for a Madison area home, your agent should separate in-district and out-of-district sales rather than blending them, as mixing the two produces an inaccurate value midpoint that serves neither seller well.

What is a list-to-sale ratio and why does it matter?

The list-to-sale ratio is the percentage of the original list price that a home ultimately sells for. A ratio of 98% means the home sold for 98 cents on every dollar of list price. In strong North Alabama submarkets like Madison, list-to-sale ratios frequently exceed 99–100%, meaning well-priced homes sell at or above asking. Ratios below 96% are a signal that homes in that area or price range are being overpriced at launch and requiring reductions to attract buyers.

How often should I expect to reduce my price if it isn’t selling?

If your home hasn’t received serious interest — showings, second visits, or offers — within the first 14–21 days, that’s a clear signal that the market is rejecting the price. A price reduction of 2–3% is typically the minimum needed to re-enter the search results of buyers who already filtered you out. One well-timed reduction executed early is far less damaging than a series of small reductions over several months, which each generate a new round of buyer skepticism.

Can I price my home based on what I paid for it plus renovations?

Unfortunately, no. The market doesn’t reimburse you dollar-for-dollar for improvements — it pays market rate for the condition and features your home presents relative to comparable properties. Some renovations yield strong returns (kitchen and bath updates, fresh paint, landscaping), while others recover very little (swimming pools in certain markets, highly personalized finishes, additions that push a home significantly above neighborhood price ceilings). Your CMA will reflect what the market actually rewards.

Your Next Step: Get a Free CMA for Your North Alabama Home

Pricing your home correctly in Huntsville, Madison, Athens, or anywhere in North Alabama starts with one thing: accurate, hyperlocal market data in the hands of an agent who knows how to use it.

What you get with a free listing consultation from North AL Property Group:

- A full Comparative Market Analysis built on the most recent comps in your specific area

- An absorption rate analysis for your price range and zip code

- A completed seller’s net sheet so you know your real bottom line before you commit to anything

- An honest assessment of what — if anything — is worth doing before you list

| Find Out What Your North Alabama Home Is Worth Get a free Comparative Market Analysis and seller’s net sheet — no obligation, no pressure.→ Book Your Free Listing Consultation at NorthALPropertyGroup.com/north-alabama-listing-agent/ |

More Resources for North Alabama Home Sellers

→ Huntsville Home Selling Timeline: How Long Does It Really Take?

→ Pre-Listing Checklist: 21 Things That Increase Your Sale Price (ROI First)

→ Seller Net Sheet Explained: What You’ll Actually Walk Away With